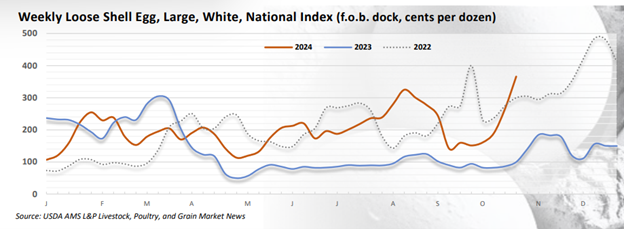

Shell egg prices have proven highly variable in the last few years. Consumer demand for eggs can be equally erratic but predictably increases around Easter in the spring and then again around the fall/winter holidays. Prices typically go up in response to this higher demand. Beginning in early summer, 2024 prices rose above and remained higher than in 2023. They spiked again in August due to lower supply caused by laying hen losses earlier in the year from Highly Pathogenic Avian Influenza (HPAI). Prices then dropped as flocks were repopulated and late summer demand fell. Now, leading up to the fall holiday season, we see egg prices spiking again, and they are higher than they were not only in 2023 but also higher than the same time in 2022. Later in 2022 wholesale egg prices reached an all-time high approaching $5.00/doz. (fig 1). When we compare 2022 to 2024, we see a haunting premonition of where egg prices could be headed this holiday season. The current price spike looks to be holiday demand coming in the face of a decrease in layers producing the eggs; the same thing we saw in 2022.

When we compare current 2024 numbers to the same timeframe in 2022 and 2023, there are a few comparable trends worth noting. Current shell egg inventory and layer numbers have dropped 13.7% and 3% respectively from the previous year, while price is significantly higher (over 300%). The current price is also 22% higher than the same time in 2022 when the egg and layer inventories were very similar to now (fig 2). It’s possible we could see the same prices on the horizon as we saw in late 2022.

While the supply and demand numbers may not bode well for egg consumers, layer producers have additional concerns. December corn is currently trading in the $4.28/bu. range and looks to stay below $4.60 through spring according to the USDA futures price estimates. This looks to be a positive for egg producers as the resulting lower feed cost could help egg producers recover from their losses as well as last year’s low egg prices – IF they have the hens to produce the eggs. The concern is that the HPAI threat still looms large over the layer industry. HPAI losses are driving the current low inventories of layers and eggs. In October of this year, 2.84 million layers were lost to HPAI to begin the holiday season. Year-to-date, the layer industry has lost 20.75 million layers, which equals 6.8% of the total current flock of producing hens. It is difficult for layer producers to keep up with current demand in the face of such losses. And now, the fall waterfowl migration is ramping up, bringing with it an increased HPAI risk. According to the USDA, there are currently only 4.1 days of shell eggs on hand for sale. Therefore, any additional hen losses could have a significant impact on the market. Whether 2024 prices will reach the highs of 2022 remains to be seen, but if HPAI continues to devastate producing layer flocks, prices this year could reach and even surpass 2022.

Figure 1: Egg prices were relatively stable, though above last year, until mid-summer, when they spiked due to laying hen losses that occurred earlier in the year. Prices spiked again this fall due to a convergence of additional hen losses to HPAI and an increasing demand for the holidays.

Figure 2: Laying hen inventory and egg inventory for 2024 looks hauntingly like 2022, when late season egg prices rose to historical levels